Lagos, NG • GMT +1

Lagos, NG • GMT +1

328 views

328 views

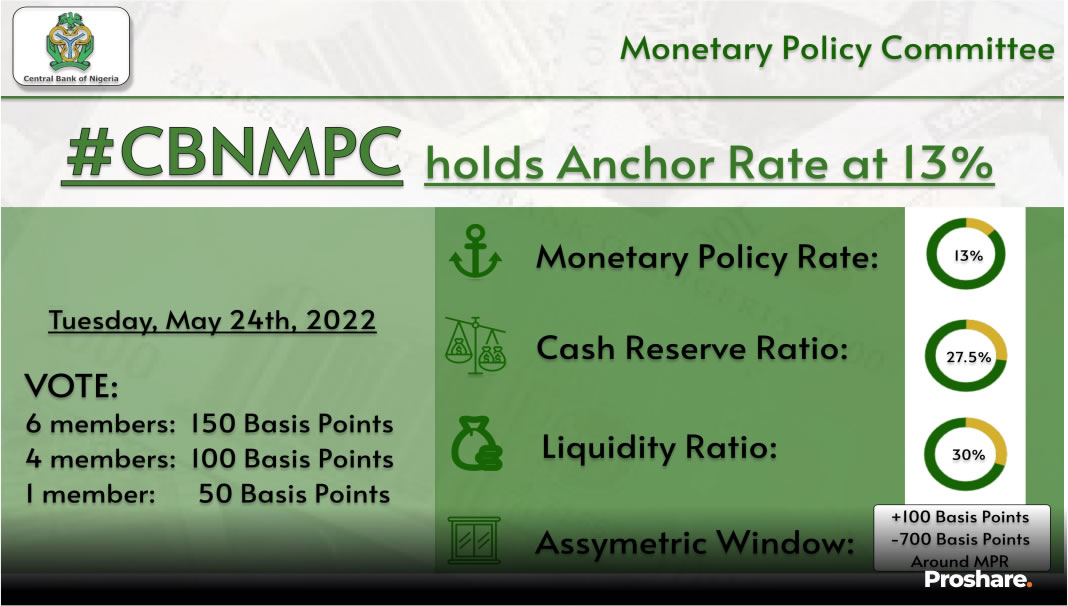

Yesterday, the CBN’s monetary policy committee (MPC) announced it had raised the policy rate by 150bps to 15.5%. The increase raises this year's total rate hikes to 400bps, making it the third straight increase. Although the decision to tighten was unanimous, members were split on the magnitude; with 10 members voting for 150bps, and 1 member each voting for 100bps and 50bps respectively. The MPC is raising rates in response to rising inflation, which is now at a 17-year high of over 20.5%. While we had expected the MPC to tighten, our expectation was for a maximum hike of c.100bps. In a bid to further tighten, the MPC increased the cash reserve ratio (CRR) by 500bps to 32.5%. All other parameters were unchanged.

The committee's justification for tightening was the need to consolidate the effects of the previous two rate hikes. Additionally, it believed that an aggressive rate increase would reduce capital outflows, possibly attract capital inflows, and strengthen the naira.

We disagree with the MPC’s latter assertion. Capital outflows have been underpinned by fx liquidity constraints and difficulties faced by the offshore community in repatriating funds rather than the level of interest rates.

On the global front, the committee underlined increased risks to the global economic recovery, which have been made worse by uncertainty arising from lingering supply chain bottlenecks due to the conflict in Ukraine and COVID-19 lockdowns in China.

It was also concerned about the impact of these factors on global trade, as well as the continued rise in global inflation, despite interest rate hikes by central banks around the world.

It emphasized the detrimental impact of another recession, particularly for fragile economies and emerging markets that are still recovering from recession, as well as those experiencing capital flow reversals due to rising yields in advanced economies.

On the domestic front, the MPC, as usual, credited the CBN's development finance initiatives and credit expansion to the private sector for the sustained positive GDP growth over the past seven quarters.

It did, however, express concern over the slowdown in economic activity as shown by the CBN's composite PMI, which dropped to 47.2 in August from 51.9 in July, indicating slower growth in the coming months.

On Inflation, the committee pointed out the steady rise in both food and core inflation, with both components rising by 110bps and 94bps m/m to 23.1% and 17.2% respectively.

Causal factors highlighted were the negative impact of rising energy prices on transportation and production costs, shocks to food supplies from widespread insecurity in the country, and the rise in monetary aggregates.

By way of implication, the rate increase is anticipated to affect the money and fixed income markets (via higher yields), further depress equity valuations, and trigger a rotation out of stocks into fixed income instruments.

The 500bps increase in CRR to 32.5% will result in tighter market liquidity, additional regulatory requirements for banks, tapering of their risk assets growth, and a negative impact on their liquidity ratios.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top