Lagos, NG • GMT +1

Lagos, NG • GMT +1

242 views

242 views

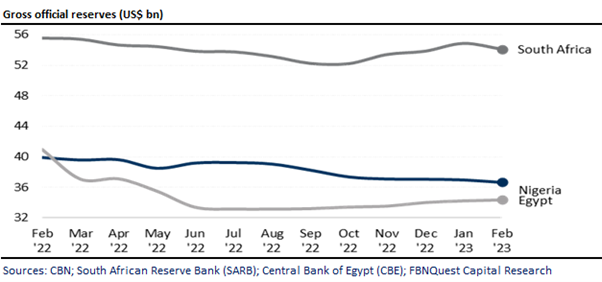

According to the CBN’s most recent data, Nigeria’s gross official reserve declined further by about -USD317m m/m to USD36.7bn in Feb ’23. As shown by our chart, with the exception of accretions recorded in the months of April, June, and July 2022, the gross official reserves have been declining steadily since Nov ‘21. Reduced foreign exchange (fx) inflow into the economy and increased demand pressure on the gross official reserves both highlight the downward trend in the reserves.

Total reserves as at end-Feb ’23 covered 7.2 months of merchandise imports on the basis of the balance of payments for the 12 months to Sep ‘22 and 5.6 months when we add services.

However, for a more accurate picture, we must adjust the gross reserve figure (and the import cover) for the pipeline of delayed external payments.

Like Nigeria, South Africa’s international liquidity position (ILP), a more comparable figure to Nigeria’s gross external reserves decreased by -USD760m in Feb ’23 to USD54.1bn.

This was mostly due to the decline in the price of gold, and valuation adjustments due to the appreciation of the US dollar.

To obtain a figure for the ILP, we add the forward position of the South African Reserve Bank to the gross reserves (which includes fx deposits and gold reserves) and then adjust the figure downward for some other less liquid component of the reserves.

In contrast, Egypt’s net foreign reserves increased by USD128m to almost USD34.4bn. In Dec ’22, the IMF approved a USD3bn extended fund facility for the country over a 46-month period to help cover its balance of payment deficit.

According to data from the Nigerian Upstream Petroleum Regulatory Commission, Nigeria’s crude oil output (including condensates) increased to 1.49 million barrels per day (mbpd) in Jan ‘23 from 1.41 mbpd in Dec ’22.

A sustained increase in oil production near historical levels may likely be favourable for the gross official reserves.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top