Lagos, NG • GMT +1

Lagos, NG • GMT +1

453 views

453 views

The NGX All-Share Index has been in correction territory for just over a month and is set to record its first quarterly fall since Q2 2021. Nigerian equity investors seem to either be ignoring this year’s solid earnings growth or demanding more earnings growth from companies

Is there still value in Nigerian stocks?

The past few months have not been rewarding for Nigerian equity investors as increasingly hawkish monetary policy and the resultant rise in market interest rates continue to dampen sentiment on the NGX Exchange. Last week, the NGX ASI fell for the third successive week and by the most in five weeks. With less than a week left in the quarter, it is now on track to record its first quarterly loss since Q2 2021 and the largest since Q1 2020.

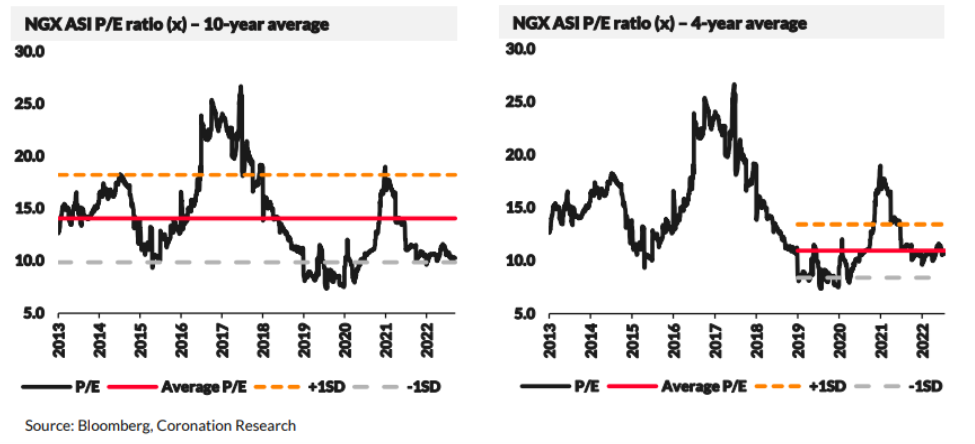

Consequently, the valuation of Nigerian equities has come-off from its recent peak, following the ongoing market correction and a 44% improvement in earnings this year. Currently, the NGX ASI is trading at a price-to-earnings (PE) multiple of 10.1x, moderating from its 2022 high of 11.6x.

In the long-term context , the PE of the NGX ASI is well below its 10-year average of 14.0x. In fact, it is 1 standard deviation below, signaling that the market is severely undervalued. In this situation, barring PE contraction below historical norms or earnings deterioration, the ASI would be expected to rise. In a shorter-term context, the NGX ASI also looks slightly undervalued compared with its 4-year average PE of 10.9x.

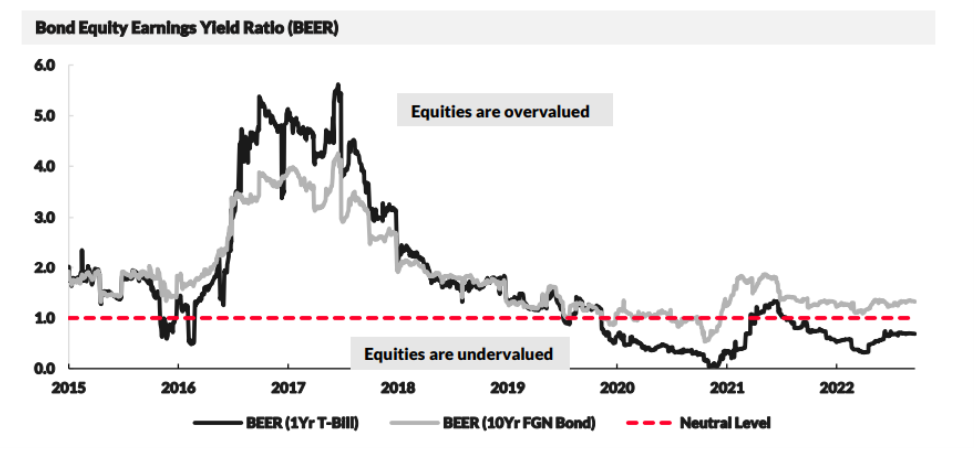

Our study on the Bond Equity Earnings yield Ratio (BEER) paints a similar picture at the moment. The bond equity earnings yield ratio (BEER) is a metric that is often used to evaluate the relationship between the earnings yield of a stock market (the inverse of the price-to-earnings ratio) relative to bonds. A number above 1 means that the equity market is overvalued, while below 1 means that equity market is undervalued.

At 0.7x, the BEER for the NGX ASI to the 1-year T-bill is at similar levels seen during most of 2020 and in the second half of 2021 when market rates were falling.

However, although the ratio is below 1, the trend in the reading has been northwards over the last few months, and with the Central Bank of Nigeria (CBN), akin to global central banks, expected to hike interest rates further to reign in inflation, valuations of Nigerian equities could see a further de-rating.

The NGX All-Share index is cheap, and valuations are likely to become more attractive in Q4 2022. As a result, we are likely to see renewed interest from long term investors, especially as earnings continue to improve (analysts' earnings expectations are up 7% since the end of June).

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.02% to close at N436.33/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) decreased by 0.42% to US$38.49bn, a 4-week low, as the CBN continues interventions across the various FX windows.

Heading into Q4, the CBN can look at its FX reserve position with satisfaction, US$38.49bn in foreign reserves being close to their historic highs and consistent with maintenance of the current I&E Window exchanges rate, or something close to it, for several months ahead. We think these conditions will continue until the end of the year, at least

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market was bearish ahead of the upcoming Monetary Policy Committee (MPC) meeting. As a result, the average benchmark yield for bonds rose 15bps to close at 12.88%. Across the curve, the yields on the 3-year (+35bps to 13.35%) and 7-year (+1bp to 12.69%) bonds expanded, while the yield on the 10-year bond was flat at 13.05%. At the FGN bond auction, the Debt Management Office (DMO) allotted a total of N261.50bn (US$599.31m), including noncompetitive allotments. Demand was weak, as reflected by a total subscription of N246.44bn and a bid-to-offer ratio of 1.10x (vs 2.78x on average in H1 2022).

Consequently, yields across the March 2025 (+100bps to 13.50%) and April 2032 (+35bps to 13.85%) bonds expanded, while the yield on the April 2037 bond closed at 14.50%. Our view remains that continued tightening by the monetary authorities and elevated Federal Government domestic borrowing will continue to drive yields upwards overthe coming months.

Activity in the Treasury Bill (T-Bill) secondary market was bullish across the curve as the average yield for T-bills fell by 15bps to 7.42%. The yield on the 258-day T-bill compressed by 1bp to close at 6.76%. At the T-bill primary auction, the DMO is expected to offer N141.34bn worth of bills. Elsewhere, the average yield for secondary market OMO bills fell by 113bps to 9.43%, while the yield on the 221-day OMO bill fell by 2bps to 11.13%

Oil

Last week, the price of Brent slumped by 5.69%, its fourth straight weekly drop and the most in many weeks, to settle at US$86.15/bbl, its lowest level since 14 January. Nonetheless, despite erasing most of this year’s gains, Brent is up 10.76% year-to-date and has traded at an average of US$102.92/bbl, 45.19% higher than the average of US$70.89/bbl in 2021.

Oil prices closed sharply lower following the 75bps rate hike by the US Federal Open Market Committee (FOMC), which brought the Fed funds rate to its highest level since 2008. This sustained aggressive stance by US Fed against inflation offset both supply-related concerns driven by the renewed mobilisation campaign in the Russia-Ukraine war and potential demand growth as China relaxed COVID-19 lockdown measures.

Nevertheless, in this exceptional year for oil prices, we maintain that prices are likely to remain above the US$73.00/bbl set in Nigeria’s government budget

Equities

Last week, the NGX All-Share Index extended its losing streak to a third week, falling by 0.91%, the most in six weeks, to settle at 49,026.62 points, the lowest level since 24 August. Consequently, its year-to-date return fell to 14.77%. Cadbury Nigeria (-13.82%), BUA Cement (-10.39%) and Guaranty Trust Holding Company (-6.09%) closed negative, while Fidelity Bank (+10.85%), International Breweries (+6.25%) and Access Holdings (+6.02%) closed positive. Performances across the NGX sub-indices were broadly negative as the NGX Oil & Gas (-4.68%), NGX Industrial Goods (-3.92%), NGX Insurance (-2.08%), NGX-30 (- 0.99%) and NGX Consumer Goods (-0.16%) declined while the NGX Banking (+2.27%) and NGX Pension (+0.05%) indices closed higher.

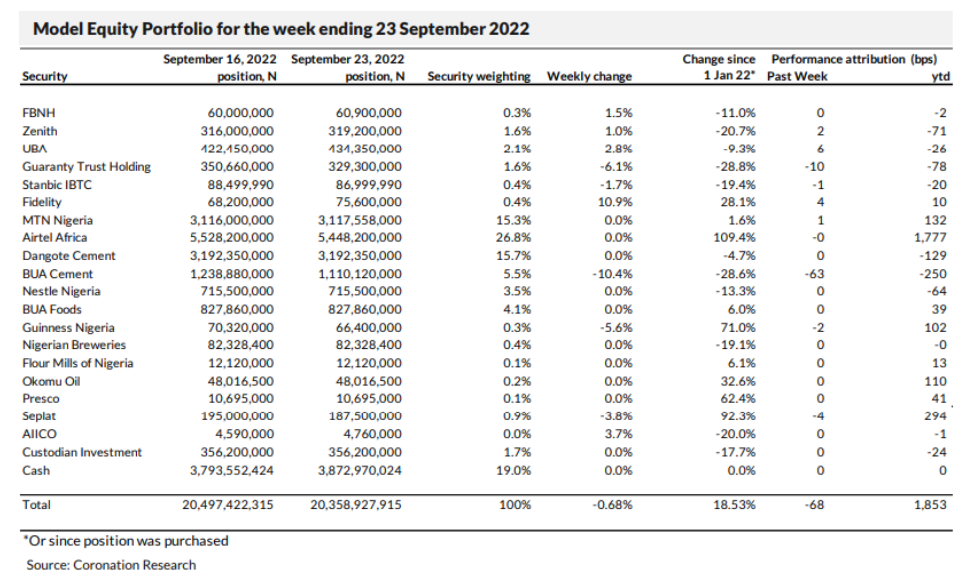

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.68% compared with fall in the NGX All-Share Index of 0.91%, outperforming it by 23ps. It has gained 18.53% year-to-date compared with a gain in the NGX-ASI of 14.77%, outperforming it by 376bps

Sector rotation is taking place in the equity market. The prices of four large index weights did not change last week, namely Airtel Africa, Dangote Cement, BUA Foods and Nestle Nigeria: but the banking index rose by 2.3%. Investors recently have shown little interest in the large telecom and industrial stocks (and BUA Cement fell by 10.4% last week), but they are interested in banking stocks, reasoning that the ongoing rise in market interest rates will translate into improved margins going forward. We have also reached this conclusion (see Coronation Research, Nigerian Banks: H1 2022 Scorecard, 19 September.) and will review our bank sector allocations accordingly.

Last week, and earlier advised, we increased our notional underweight position in Airtel Africa to almost 200bps by making notional sales in the stock. Going forward, we are considering re-balancing the portfolio away from the major telecom and industrial stocks and towards banks. We will report back next week. In the meantime, plan no changes this week.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top