Lagos, NG • GMT +1

Lagos, NG • GMT +1

3608 views

3608 views

"If banks cannot truly be customer intimate, they are doomed to be just dumb commodities, acting behind the scenes, like utilities."

-JP Nicols, bank innovation expert

Nigerian Banking Industry- The Evolution

Nigeria's banking system has undergone various transitions, especially over the last 22 years, from 89 banks before 1999 to the universal banking regime that commenced in earnest in 2000 and then onto the consolidation of 2005. Between 2005 and 2010, the number of banks collapsed to 25 larger institutions with a stronger capacity to support big-ticket domestic transactions and support manufacturing and service sector growth. The period was disruptive but progressive. In 2010 another round of consolidation took place, creating even larger banks. The "great consolidations" were expected to develop a few of Africa's largest banking franchises, but this is yet to happen. The steady depreciation of the Naira and the rising non-performing loans as banks became bigger hobbled their growth.

The Tier 1 bank classification as defined by Afrinvest in its 2013 special Banking report was made within a context. So much has changed ever since. At the time, the Nigerian banking ecosystem was characterized by several features. The changes it has seen have been far-reaching, affecting not just the regulators, operators but also customers. Back in 2013, when the Afrinvest model was formulated, even the largest Nigerian Banks in Asset size could not boast of Assets worth N5tr. As of 2021 about half of the quoted banks have assets in excess of 5tr.

Another current reality that marks a major difference between the banking industry today and what was obtained in 2013 is the fact that back then there was a finite number of operators, today’s banking industry has an elastic and almost infinite universe of banks. Whereas in 2013, Banks identified as such, today’s banks are increasingly less identifiable by their titles and so non-traditional banking institutions holding the requisite license abound. The rise of Digital Banks like Kuda, Opay, Palmpay, Fairmoney and a host of others has redefined the banking landscape. Likewise, Payment Service Banks (PSBs), Telecoms companies like MTN and Airtel have also recently obtained full approval from the regulator to operate as payment banks. Microfinance Banks and community banks led the financial inclusion agenda of the government a decade ago whereas, PSBs approvals have become a major driver of financial inclusion (see illustration 12 below).

Illustration 12: The Evolution of Nigerian Banking system

The incursion of PSBs has generated mixed reactions from traditional banks. While some banks have regarded the rise of PSBs as a threat to their operations and earnings others seem to have however identified opportunities. Such banks are showing increasing interest in owning, partnering, or even acquiring PSBs. Whereas the fact that most Nigerians prefer to keep their savings in checking accounts suggests that such accounts are actually meant for payments. Payments Banks recognizing this have therefore chosen to create an alternative that is less costly but as efficient as conventional banks. Conventional commercial banks however can capitalize on the rise of PSBs not just by providing clearing services for the PSBs (since they are not licensed to do so) but as has been the case banks can set up PSBs altogether. So, while the banks may generally hold lower deposits, they can earn commissions on clearing for the PSBs thereby diversifying their P&Ls (see illustration 13 below).

Illustration 13: Nigerian Banks and Disruptive Incursion of Payment Banks

As noted later in the report, Nigerian banks are still significantly smaller than their South African and Egyptian counterparts. It would be difficult to urge bank recapitalization in a difficult economic situation. Still, at some point, the financialization of assets would be called upon to enhance the capital size of domestic banking institutions.

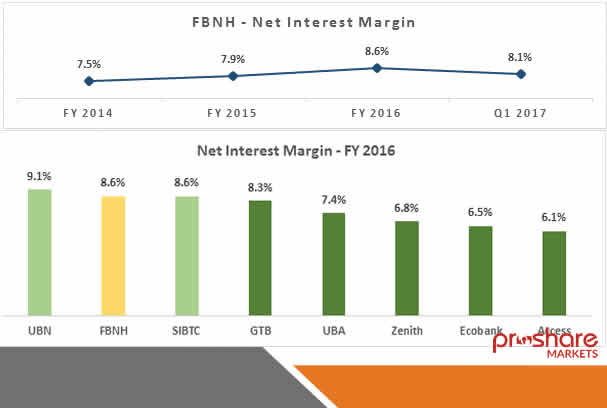

Nigeria's banking sector rotates around two circles of bank types called tier 1 and 2. Before now, the Tier 1 banks had the largest loan assets and deposits, showed the strongest levels of operational efficiency and highest returns on shareholders' funds. The second-tier banks were contextually less strong than their tier-one counterparts, but this may not be true for every aspect of their businesses. For example, a few tier 11 banks have shown greater skill and agility in growing their digital banking income relative to gross earnings.

Downloadable Versions of Tier 1 Banks Report (PDF)

1. Executive Summary: Nigeria’s Banking Industry: The Case for Redefining Tier 1 Banks - May 28, 2022

2. Full Report: Nigeria’s Banking Industry: The Case for Redefining Tier 1 Banks - May 28, 2022

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top