Lagos, NG • GMT +1

Lagos, NG • GMT +1

271 views

271 views

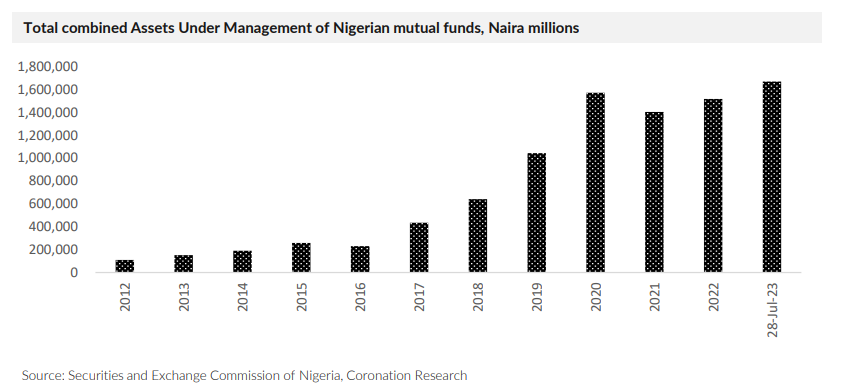

In all the turmoil of 2023 there are some surprises. One of these is the health of the Mutual Fund industry, which grew its total assets under management (AUM) by 10.1% during the first seven months of the year. Better than that, the total AUM of Money Market funds grew by 30.1% in seven months, adding N191.4 billion. What explains the new growth of Mutual Funds?

The Surprising Growth of Mutual Funds

For most of this year market interest rates have been unappealing, and, in any case, savers have been under pressure from rising inflation. Under these circumstances, one would expect Nigeria's Mutual Fund industry to have declined. Right?

Wrong. The Mutual Fund industry grew by 10.1% during the seven months to the end of July 2023 adding a total of N152.8 billion of assets under management (AUM). This compares with growth of just 8.1% for the full-year 2022 and a decline of 10.6% in 2021. Even though growth of 10.1% over seven months does not beat the rate of inflation, it is a remarkable performance against the odds

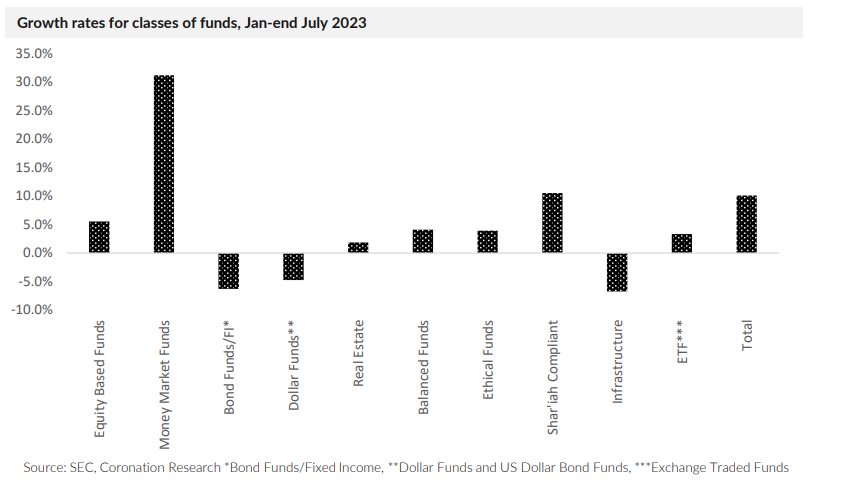

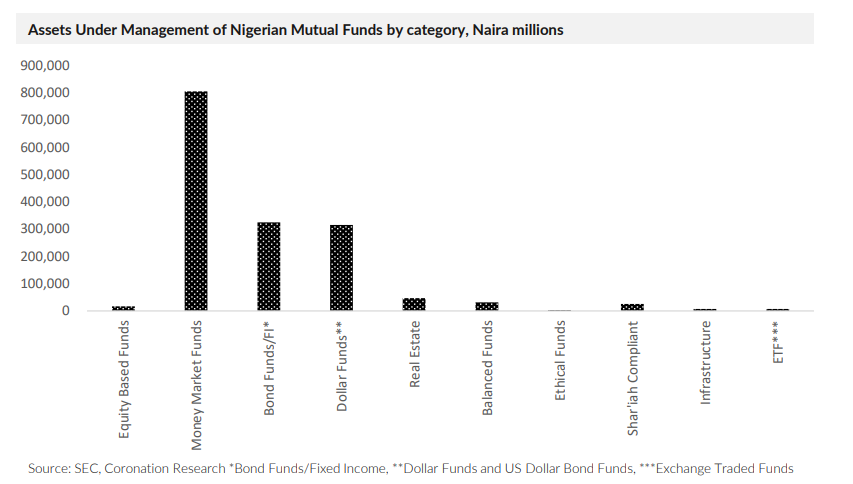

Data from Nigeria's Securities and Exchange Commission (SEC) show that Money Market funds were the driving force. They grew by 30.1% during the seven months to July, adding N191.4 billion of assets under management. Of 29 SECregistered Money Market funds, 27 grew during the first seven months of this year, 12 of them growing by more than 20%. Growth of assets under management easily outstripped the rate of inflation.

The only other class of fund to record significant growth were Shariah Compliant funds which grew by 10.5% during the first seven months of the year.

What explains the growth of Money Market funds? One reason is the very low yields offered on bank deposits early in the year. The banknote withdrawal policy meant that banknotes flooded into the accounts of banks in January, making them extremely liquid. Liquid banks do not need to offer their depositors much in the way of interest rates. Even though Nigerian Treasury Bill (T-bill) rates were low at the time, they were attractive relative to what banks were offering. So Money Market mutual funds, which have large holdings of T-bills, offered much better rates than bank deposits

And what of the future? Banks are becoming more liquid, thanks to ongoing reforms that remove some of the restrictions imposed on them over the past four years (see Coronation Research, Investment Opportunities from FX Liberalisation, 11 July). And market interest rates appear to be moving upwards. We know that Money Market funds compete with banks for deposits, so the bigger the difference between banks' deposit rates and market interest rates the better for Money Market funds. And Money Market funds account for just over half the total assets under management of the industry. The prospects for the industry are improving.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 0.15% to close at N739.60/US$1. In the parallel (or street) market, the Naira gained by 11.05% to close at N860.00/US$1. Currently, the gap between the I&E Window and the parallel market stands at 13.00%. The gross foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) slipped by 0.15% to US$33.82bn.

Earlier last week, the Nigerian National Petroleum Company and Afreximbank signed a term sheet for a $3.0 billion loan for the repayment of crude oil and to support the Federal Government with its ongoing fiscal and monetary policy reforms. This seems to have brought some stability to the FX market. In the medium term we maintain that the reforms in the foreign currency market will lead to improvements in FX liquidity.

Bonds & T-bills

Last week, the secondary market for T-bills remained bearish with average yields increasing by 106bps to 8.39% pa. Average yields along the T-bill curve increased: at the short end (190bps to 6.59%); mid-end (151bps to 7.86%); and long end (65bps to 9.41%).

At the FGN bond auction, the Debt Management Office (DMO) offered N360.00bn across the April 2029 (bid-to-offer: 0.15x), June 2033 (bid-to offer: 0.06x), June 2038 (bid-to-offer: 0.55x) and June 2053 (bid-to-offer: 2.71x) maturities with most of the demand skewed to the 30-year bonds. Demand was lower than at the last auction in July, as reflected by a total subscription of N312.56bn (N945.14bn at the last auction) and a bid-to offer ratio of 0.87x (vs 2.63x at the last auction). Yields increased across all tenors with the 6-year bond up by 205bps to 14.55%, the 10-year bond by 110bps to 14.70%, the 15-year bond up by 135bps to 15.45%, and the 30-year bond up by 140bps to 15.70%. A total of N230.26bn was eventually allotted, including non-competitive allotments of N2.50bn. The secondary market for FGN bonds moved in the same direction. The average yield increased by 309bps to 13.83%. Average yields along the FGN bond yield curve rose: at the short end (46bps to 12.00%); mid-end (25bps to 13.85%); and long end (26bps to 15.18%).

It seems that the market is heading towards a new period of elevated rates, if the OMO auction two weeks ago and last weeks’ bond auction are reliable indicators.

Oil

Last week, the seven-week rise in oil prices was interrupted as Brent closed on a negative note, retracting by 2.32% to settle at US$84.80/bbl. Brent is down by 1.29% year-to-date and is trading at an average of US$80.46/bbl year-to-date, 18.80% lower than the average of US$99.09/bbl in 2022. The future course of crude prices will likely depend on whether China - the single largest importer of crude oil globally - is able to maintain demand or whether its housing sector problems and price deflation will lead it in the direction of recession. We maintain our view that, for most of the year, prices are likely to remain above the US$75.00/bbl mark set in Nigeria’s government budget

Equities

Last week, the NGX All-Share Index closed lower, decreasing by 0.93% to settle at 64,721.09 points. Its year-to-date return declined to 26.28%. Unilever Nigeria (-7.05%), Honeywell Flour Mills (-5.88%), and Okomu Oil Palm (-5.66%) closed negative while Dangote Sugar (+6.06%), International Breweries (+4.44%), and BUA Foods (+4.40%) closed positive. Performances across the NGX sub-indices were mostly negative as NGX Insurance (-2.17%) topped the list, followed by, NGX Banking (-2.06%) and NGX Oil/Gas (-1.13%) indices closing red. On the other hand, the NGX Consumer Goods (+2.39%) and the NGX Industrial Goods (+0.37%) indices closed in the green.

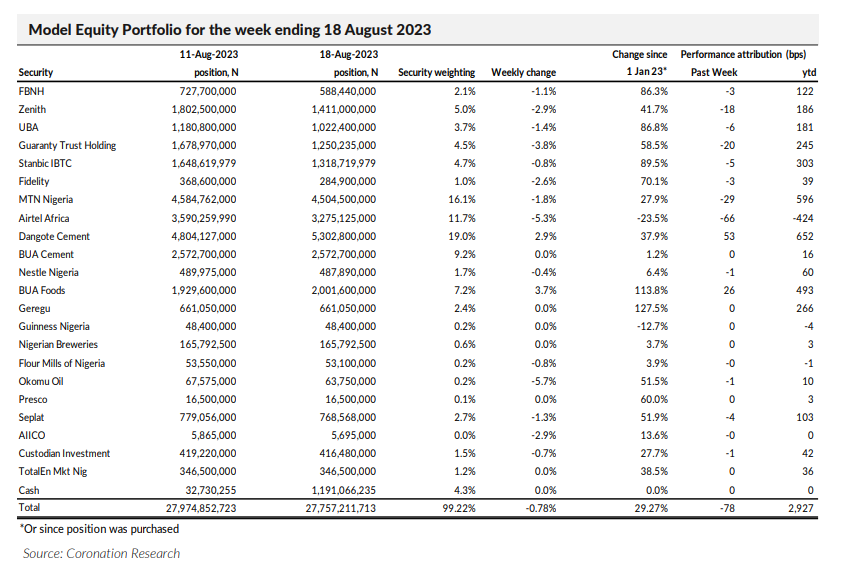

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.78% compared with a fall in the NGX All-Share Index of 0.89%, outperforming it by 11bps. Year-to-date it has risen by 29.27% compared with a rise of 26.33% in the NGX All-Share Index, outperforming it by 294bps.

Last week we wrote that we believe that much of the upside in banks has been priced in, the NGX Banking Index having risen by 63.6% year-to-date compared with its 73.7% gain in full-year 2017, the last year when a dual-exchange rate system was ended. Though we continue to look forward to excellent Q3 and full-year results, we took the decision, last week, to make notional sales across our nearly double-overweight position in the banks in order to bring our overall banks position to below a neutral weight relative to the index.

So, last week we began work on this and made notional sales in each of our bank holdings, bringing the total sector exposure down from 26.5% of the Model Equity Portfolio to 21.0%. This is still 40% higher than a neutral weight so we will continue with these notional trades over the coming weeks. We will also, once again, carefully measure our exposure in the top-five stocks by market capitalisation and align with neutral notional positions in them.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top